The Money Laundering and Asset Recovery Section of the USA Department of Justice in court Case 2:17-CV-04438 filed in US Central District of California [1] established a link between the 1MDB scandal and the $2,200 million dollar purchase of Houston based Oscar Wyatt’s company Coastal Energy Resources [2,3]. The valuation of Coastal at the time of the purchase by a CEPSA-Jho Low partnership created for this purpose in January 2014 was entirely based on Coastal’s claim of the existence of 66 Million barrels of proved reserves in assets [4,5]. Using the Thailand Department of Mineral Fuels Annual Reports between 2008 and 2018 to examine Coastal production data [6], which was not publicly available 4 years ago, one can show that around 45 million barrels of Coastal’s proved reserves were fictitious, or in other words, were fabricated in order to inflate the value of Coastal before the purchase by CEPSA.

In April 2019 two news articles both connected to the company Coastal Energy Resources were published that can finally help us to shed some light on the true nature of the 1MDB scandal. The first one, which was echoed by the international press, was the purchase of 37% of CEPSA by the Carlyle Group [7]. The second seemingly irrelevant event had taken place just a couple of days earlier. CEPSA’s owned Coastal Energy Resources announced that it had awarded the decommissioning contract of Songkhla oilfield two wellhead platforms and their connection bridge in the Gulf of Thailand’s offshore block G5/43 to a consortium between the Thai company Unithai Shipyard & Engineering and the Chinese Offshore Oil Engineering company COOEC [8].

This brief press release went completely unnoticed in the international press in spite of the fact that the Songkhla oil field was the main asset in 2014 Oscar Wyatt’s sensational $2.2 billion sale of 1MDB connected Coastal Energy Resources to Emirati owned Spanish oil corporation CEPSA [9,10].

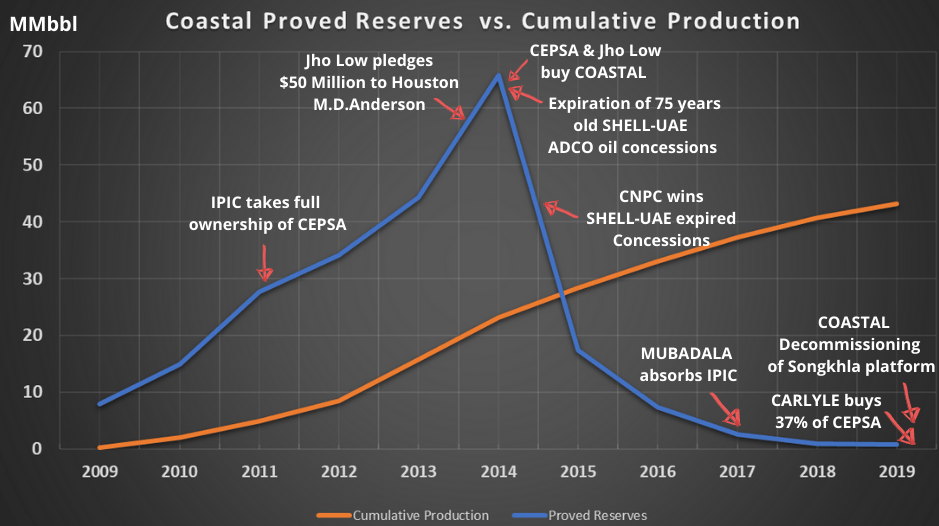

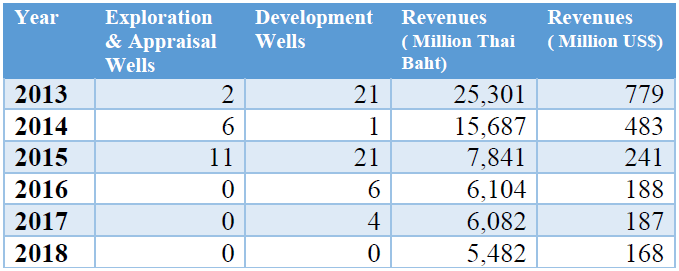

According to the Thailand Department of Mineral Fuels (DMF) Annual Reports between 2008 and 2018 the company Coastal Energy Resources (CEC International in the Thailand DMF Reports) declared before the sale to CEPSA 66 MMbbl (million barrels) in proved reserves. Surprisingly by the end of 2014, less than one year after the sale, Coastal declared to the Thai DMF proved reserves of only 17 MMbbl (Million barrels). Since the cumulative production for the year 2014 was only 5 million barrels this implies that nearly 45 million barrels in proved reserves disappeared in thin air (see Figure below). At $50 per barrel, this unaccounted decline in reserves amounts to the entire valuation of Coastal at the time of the CEPSA purchase.

Some may argue that CEPSA is to blame for not having performed due diligence in their internal and third-party independent valuation of Coastal assets before the purchase. One may also be tempted to think that the sudden decline in Coastal’s proved reserves was an unintentional technical mistake or perhaps an unexpected event connected to the 2014 rapid decline in the price of the barrel of crude. I will show that this is not the case. We must keep in mind that the declaration of proved reserves by Oil & Gas companies is a business strictly regulated by government agencies all over the world. In this case, the Thai DMF and the Spanish CNMV (Comision Nacional del Mercado de Valores), which are the equivalents of the USA SEC, had to oversee the declared proved reserves and had to approve the Coastal-CEPSA deal respectively.

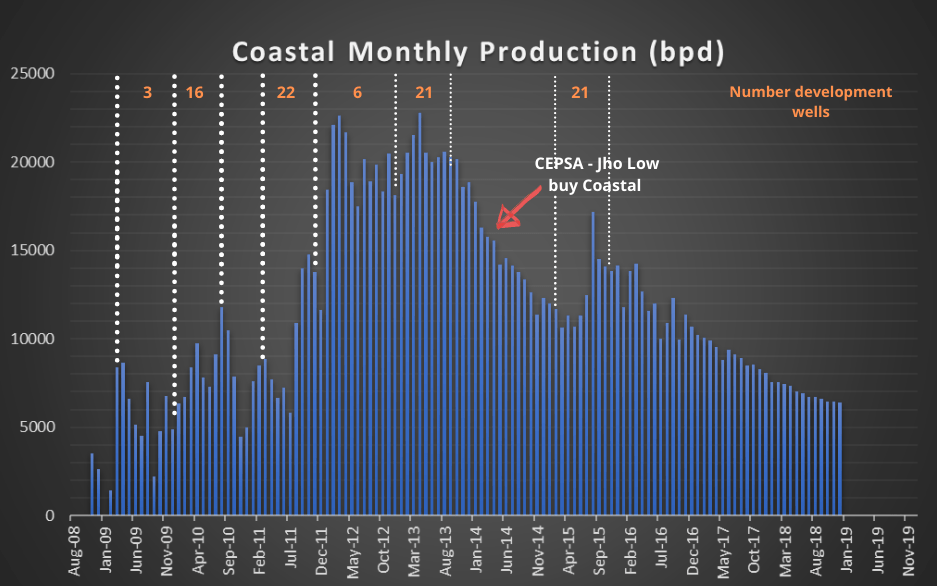

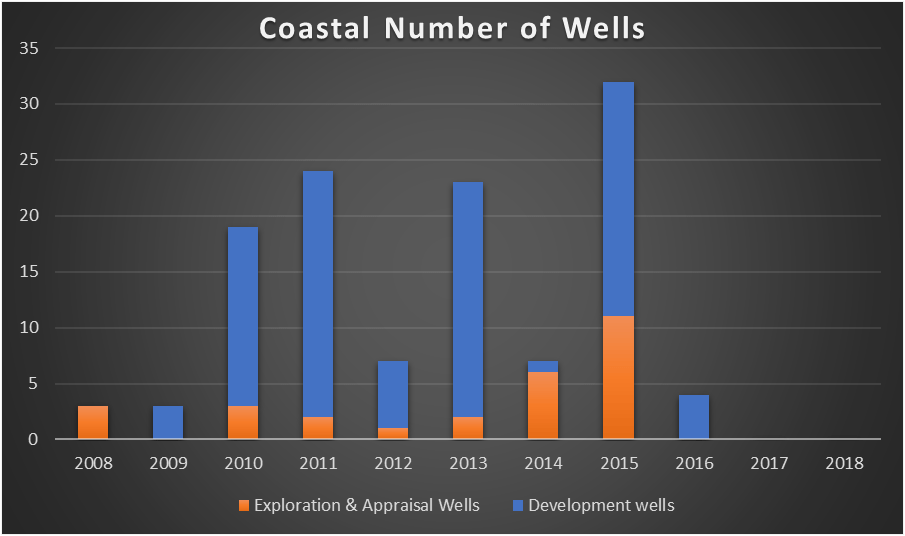

A closer look at the publicly available monthly production data for Coastal Energy in Thailand between 2008 and 2018 [6] shows that by the time of the Coastal-CEPSA deal on January 2014 Coastal’s production was clearly more than half a year in rapid decline (see Figure below). This fact must have been obvious for all Coastal, IPIC as well as CEPSA technical experts. They must have noticed that the 21 development wells that Coastal drilled in the first half of 2013 only served to keep production stable at around 20,000 bpd for only a few months, which was used as the basis to overestimate the proved reserves, and therefore that the supposed 66 million barrels of proved reserves claimed by Coastal were a gross overestimation [4,5].

In 2015 after having declared 17 MMbbl of proved reserves Coastal, now under full CEPSA ownership, embarked in a campaign of exploration and appraisal drilling 11 exploration and appraisal wells and 21 production wells. The production increased briefly for a few months from 12,000 bpd by the end of 2014 to around 15,000 bpd by the end of 2015 only to resume the previous rapid decline in full force. By the end of 2015, Coastal declared only 7.5 million barrels of proved reserves to the Thai DMF and would only drill 6 additional wells in the concession before decommissioning in April 2019.

In July 2018 CEPSA commissioned an independent analysis of its assets to Louisiana based Petroleum Consulting company Rydler Scott [11] including the offshore oilfields in the Gulf of Thailand. Rydler Scott consultants concluded that all Songkhla platforms were no longer producing and in simple words that the Songkhla assets were basically a liability that would have to be decommissioned by 2019 at a cost of approximately $60 million dollars [11].

Rydler Scott’s conclusions stand in stark contrast with the Reserves Report [4,5] that Coastal Energy Resources commissioned in 2013 to Houston based energy consulting firm RPS (Reserves and Contingent Resources). The unsigned final draft of RPS’s Coastal 2013 Reserves Report [5] and the signed 2012 Reserves Report [4] are available for public download from Coastal’s website.

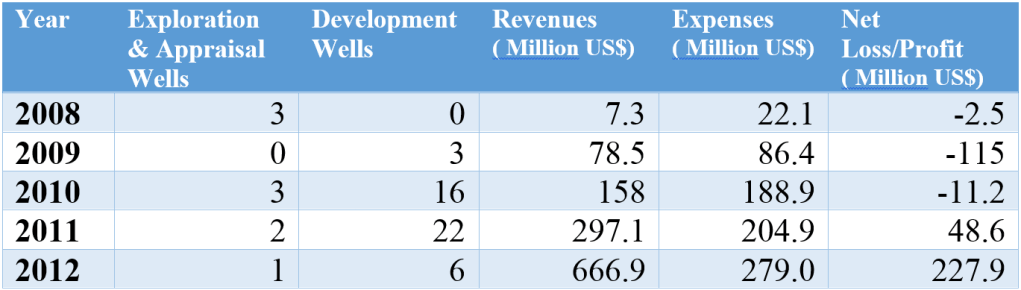

We know from Coastal corporate Annual Reports between 2008 and 2012 [12] that Coastal accumulated net losses between 2008-2010 of approximately -$130 million and net profits between 2011-2012 of approximately +$275 million. We do not know Coastal expenses in 2013 and onward but we know Coastal revenues before paying royalties to the Thai government between 2013 and 2018 from the Thai DMF Annual Reports. If we assume the same expenses and royalty levels in 2013 than in 2012 and trust the production numbers Coastal reported to the DMF we can estimate that Coastal net profit in 2013 just before the sale to CEPSA must have been around $260 million.

We can make an optimistic estimation of Coastal net losses after the purchase by CEPSA. If we assume for instance that the expenses were similar to the expenses in 2012 and add around $60 million in decommissioning costs we estimate that CEPSA accumulated more than $100 million in net losses between January 2014 and April 2019. One may wonder how the financially disastrous purchase of Coastal has impacted CEPSA valuation.

In February 2011 UAE’s sovereign wealth fund I.P.I.C, which would be absorbed by Mubadala in 2017, acquired full ownership of CEPSA paying US $5.37 billion dollars for the 53% of the company that did not already own. This implies that IPIC had valued CEPSA on early 2011 at approximately US $10.2 billion dollars. If we adjust for inflation this 2011 valuation translates in $11.9 billion in 2019 dollars. If we take into account the US$300 million in fees paid to the middleman Jho Low after the acquisition of Coastal we conclude that CEPSA lost by our estimations close to $3,000 million dollars therefore the valuation of CEPSA on 2019 should have been only around $9 billion US dollars.

Amazingly on April 9th 2019, only one day after CEPSA owned Coastal announced the decommissioning of its offshore platforms in Thailand [8] the largest Private Equity firm in the world, the Carlyle Group, announced the acquisition of a 37% stake in CEPSA for US $4.8 billion, which implies that Carlyle valued CEPSA at an astounding US $12.9 billion [7], a US $4 billion gift to Mubadala that defies double accounting logic.

References :

[1] United States of America, Plaintiff v. Certain Rights to and Interests in the Viceroy Hotel Group, Defendant. No CV 17-4438 Verified Complaint for Forfeiture In REM [18 U.S.C. 981(a)(1)(A) and (C) [F.B.I.] (USA District Court for The Central District of California)

[2] US Lawsuit Links $2.2 billion deal to Malaysian 1MDB scandal (June 12th 2017, Tom Wright, Justin Baer, Bradley Hope, Washington Street Journal) . It is well known by now that Jho Low partnered with emirati owned Spanish oil company CEPSA to buy Coastal using $50 million dollars that originated in the 1MDB fund. Just one week after the purchase Jho Low sold his $50 million initial share of Coastal to CEPSA for $300 million.

[3] Jho Low’s Texas Energy Deal Scrutinized (June 13th 2017 FiNews.com).

[4] Offshore Reserves Songkhla Field and G5/43 Concession Economic Evaluation (January 1st 2013, prepared for Coastal Energy by RPS). This Coastal Report is publicly available for download at Coastal website, www.coastalenergy.com

[5] Songkhla Field and G5/43 Concession Economic Evaluation (January 1st 2012, prepared for Coastal Energy by RPS)

[6] Thailand Department of Mineral Fuels 2008 Annual Report; 2009 Annual Report; 2010 Annual Report; 2011 Annual Report; 2012 Annual Report; 2013 Annual Report; 2014 Annual Report; 2015 Annual Report; 2016 Annual Report; 2017 Annual Report; 2018 Annual Report (Thailand Ministry of Energy). These documents are available for public download at www.dmf.go.th

[7] Carlyle to buy up to US $4.8 billion stake in CEPSA from Abu Dhabi’s Mubadala (April 8th 2019, Reuters Business News); Carlyle Group to buy up to 40% stake in Spanish oil company from Mubadala (April 8th 2019, CNBC)

[8] UniThai-COOEC Consortium wins Gulf of Thailand Decommissioning Gig (April 11th 2019, IHS Markit, Connect Upstream Insight)

[9] CEPSA finalizes Coastal Energy Takeover (January 20th 2014, Offshore Energy Today).

[10] Texas Oil Legend Oscar Wyatt Hits $500 Million Payday in deal with Malaysian investor (Nov 19th 2013, Forbes)

[11] Competent Person’s Report – Escalated Parameters – CEPSA (July 1st 2018, Ryder Scott Petroleum Consultants)

[12] Coastal Energy 2007 Annual Report (Dec 31st 2007), Coastal Energy 2008 Annual Report (Dec 31st 2008), Coastal Energy 2009 Annual Report, Creating Value through Organic Growth (Dec 31st 2009), Coastal Energy 2010 Annual Report, Production, Profits, Potential (Dec 31st 2010), Coastal Energy 2011 Annual Report, The Path to Performance (Dec 31st 2011), Coastal Energy 2012 Annual Report, New Directions, New Opportunities (Dec 31st 2012). Coastal Energy Annual Reports from 2007 to 2012 are publicly available for download at Coastal website, www.coastalenergy.com

Make a one-time donation

Make a monthly donation

Make a yearly donation

Choose an amount

Or enter a custom amount

Your contribution is appreciated.

Your contribution is appreciated.

Your contribution is appreciated.

Categories: Reserves Fraud